Collections

What Is a Credit Lock and How Does It Work?

March 11, 2026

Does Credit Repair Hurt Your Credit Score?

Credit Scores

VantageScore 4.0: Your Complete Guide to This Credit Model

Mortgage Credit Reporting: What Borrowers Need to Know

How to Work on Improving Your Credit Score

How to Raise Your Credit Score: Strategies That Work

Credit Repair

Credit Card Delinquency: Your Complete Recovery Guide

How Do Debt Collections Affect Your Credit Score?

March 9, 2026

How to Get All Three Credit Reports

How to Qualify for an Apartment With Bad Credit

What Is a Credit Lock?

How to File a Complaint Against a Credit Repair Company

How Does Debt Settlement Affect Your Credit?

Why a Great Credit Score Is Vital to Getting a Mortgage

How to Remove Medical Debt From Credit Reports

Credit Saint Named Best Credit Repair Company

February 10, 2026

How to Improve Your Credit Score Safely: A Complete Guide

February 4, 2026

Minimum Credit Score Needed to Buy a House in 2025

July 23, 2025

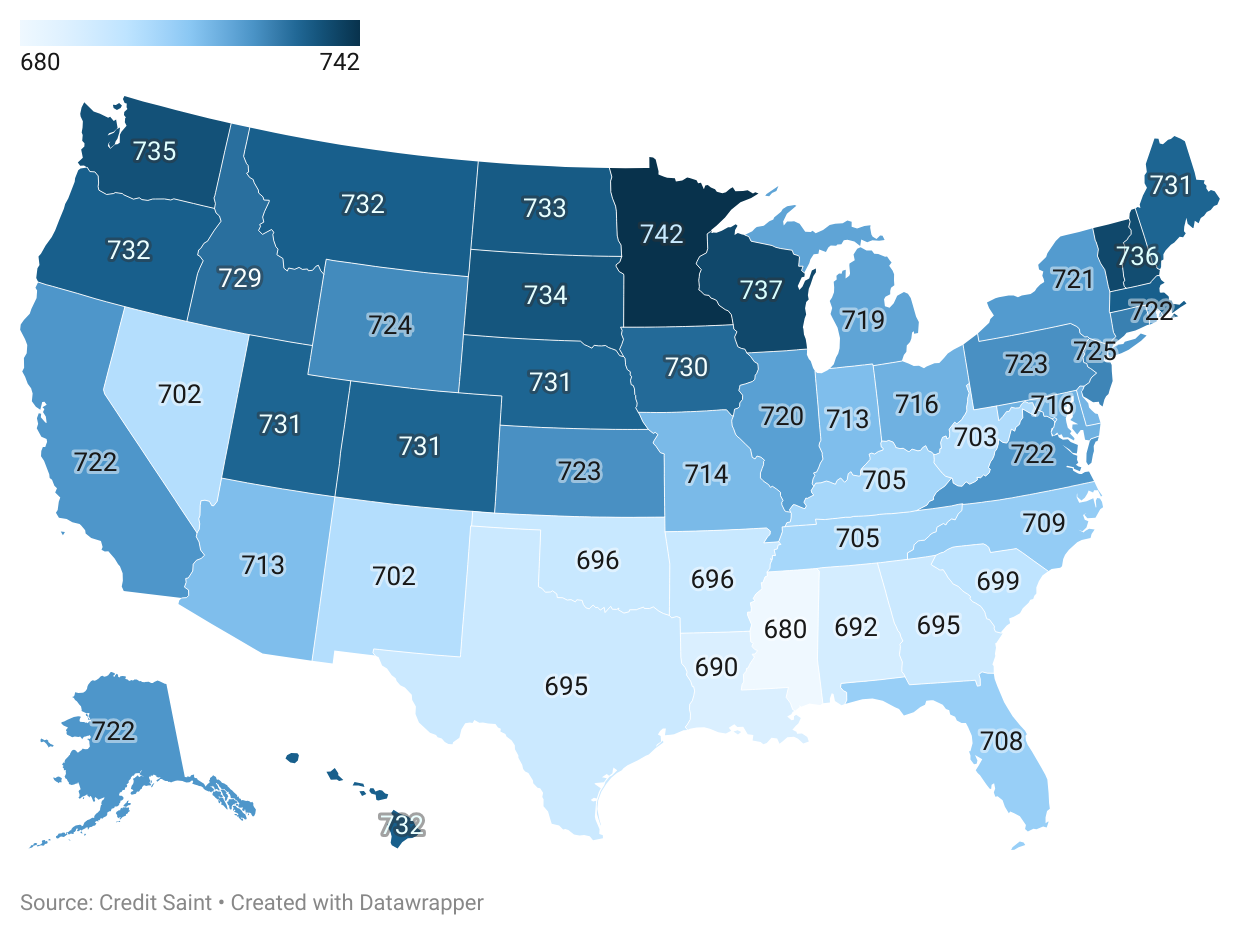

What is the Average Credit Score by State?

August 21, 2024

Local Services

Credit Repair in Texas

August 23, 2024

Credit Repair in Florida

August 22, 2024

How Debt Collection Works

October 12, 2023

Credit Repair for Couples

August 12, 2024

Repairing Credit After Identity Theft

August 8, 2024

Credit Counseling vs Credit Repair

August 5, 2024

How to Use Balance Transfer Cards for Credit Repair

July 30, 2024

Credit Utilization: How It Affects Your Credit Score

December 29, 2023

How to Remove Inquiries from Your Credit Report

November 29, 2023

When Do Collection Agencies Report to Credit Bureaus?

December 14, 2023

Credit Scores: How They Work and Why They Matter

November 22, 2023

Preparing Your Credit for a Major Purchase

April 12, 2024

How to Remove Repossessions from Your Credit Report

October 24, 2023

What Is a Judgment and Will It Hurt Your Credit?

How to Remove Late Payments from Your Credit Report

October 17, 2023

How to Remove Foreclosures from Your Credit Report

October 26, 2023

How Long Do Collections Stay on Your Credit Report?

February 1, 2024

How to Increase Credit Score Quickly

January 3, 2024

New Jersey Credit Repair

December 19, 2023

How to Remove Bankruptcies from Your Credit Report

October 27, 2023

How to Remove Collections from Your Credit Report

How to Dispute Items on Your Credit Report

October 13, 2023

How to Write an Effective Credit Dispute Letter

November 13, 2023

The Price You Pay: 6 Side Effects of Bad Credit

December 16, 2023

Understanding Credit Repair Companies

What to Do if a Debt Collector Never Sent a Written Notice

December 15, 2023

How to Remove Charge-offs from Your Credit Report

October 18, 2023